Design Risk Prediction Services That Actually Guide Decisions

Reframe risk prediction services from raw scores to decision-support engines that pair calibrated probability ranges with clear, auditable actions.

Most “advanced” risk prediction services quietly fail in the same way: they stop at a score. Dashboards look impressive, model AUCs are polished into slideware, but front-line teams still ask the same question—“So what do we actually do at 0.63 risk?” Until probability ranges are tied to explicit decisions, playbooks, and workflows, risk prediction is an expensive awareness exercise, not a decision engine.

If you’ve invested in risk prediction models and still see inconsistent decisions, stalled AI value, and frustrated risk and operations leaders, you’re not alone. The gap isn’t usually the modeling; it’s the translation layer between prediction and action. The organizations that win treat risk analytics as part of a broader decision support system, not as standalone tooling.

In this article, we’ll outline a practical blueprint for designing and choosing risk prediction services that actually guide decisions. We’ll move from calibrated probability ranges to guidance patterns and workflow integration, and we’ll close with how we at Buzzi.ai build AI-powered, decision-centric risk prediction solutions. The goal is simple: help you turn predictive risk analytics into repeatable, auditable, and ultimately more profitable decisions.

From Risk Scores to Decisions: What Risk Prediction Services Should Do

Most teams first encounter risk prediction services as a scoring feature. A model ingests historical data, spits out a risk score, and that score shows up in a report, dashboard, or API response. Useful in theory, but unless those scores are embedded into how decisions are made, they remain another line in a spreadsheet.

What risk prediction services are—beyond risk scoring tools

At their best, risk prediction services are end-to-end capabilities. They ingest data from multiple systems, run one or more risk prediction models, and surface outputs directly into the tools where people or systems decide what to do next. They don’t end at risk scoring; they close the loop from data to decision.

Think of a loan underwriting setup. A simple risk scoring tool just shows a score on screen: “Applicant risk = 0.27.” An actual decision support system goes further: it uses predictive risk analytics to stratify the applicant into a band and suggests an explicit action: “Approve with standard terms,” “Approve with higher rate,” or “Decline, request additional documentation.”

That’s the key distinction. Traditional tools generate numbers and leave humans to improvise. A modern decision-supporting service couples the predictions with rules, playbooks, and interfaces that guide actions. In practice, that means aligned operational workflows where scoring is only one component of a broader decision fabric.

Why raw risk scores are insufficient for effective decision making

Raw scores feel precise but create a cognitive gap. Humans are not great at mapping abstract values like “0.63 risk” or even “63% probability” into consistent, context-aware choices. So they fall back to habits, local norms, or gut feel.

This shows up in familiar failure modes. Dashboards of “actionable insights” that no one logs into. Teams where a 0.78 risk score leads to approval on Monday and denial on Tuesday, depending on who’s on shift. Fraud or compliance functions where senior analysts override models based on intuition, leaving governance risk and compliance teams uneasy about undocumented logic.

Consider a fraud team viewing a transaction labeled 0.78 risk. One analyst blocks it. Another sends a one-time password. A third lets it through because “the customer is VIP.” When an audit lands, there’s no clear reason why similar cases were handled differently. The problem isn’t the model alone; it’s the absence of structured risk-based decision making connected to the scores.

Reframing risk prediction as decision support, not model output

The unit of value here is not a better ROC curve; it’s a better decision. A decision is better when it reduces loss or incidents, improves customer outcomes, or makes operations more efficient, ideally measured over time. That requires a different mental model for how we design risk prediction services.

A decision-centric view combines several layers: calibrated probability ranges; clearly defined decision thresholds; reusable guidance patterns; and deep operational workflows integration. The prediction is just the raw material for the decision support system.

Imagine two teams using the same model with identical accuracy. Team A shows the score in a dashboard and tells analysts to “use it as one input.” Team B defines bands, maps them to explicit actions, routes work automatically, and tracks outcomes by band. Team B will get far more ROI—not because their predictive analytics are smarter, but because the predictions are wired into how work actually gets done.

Designing Risk Prediction Models for Probability Ranges, Not Binary Flags

If we want risk prediction services with probability ranges and action guidance, we need to design the models differently from the outset. The goal isn’t “tell me yes or no,” but “tell me how likely a bad outcome is so I can choose the right playbook.” That means modeling for probability ranges instead of only chasing a single binary cutoff.

Why probability ranges beat single thresholds

Many early systems are built around a single hard threshold: approve below 0.6, decline above. This binary framing hides uncertainty and kills flexibility. It forces all the nuance of your risk stratification into one brittle line.

Probability ranges are a better fit for decision-centric design. You might define bands like 0–5%, 5–20%, 20–50%, and 50%+ predicted risk. Each band can then link to a different mitigation intensity or workflow, enabling richer scenario analysis and more tailored risk mitigation strategies.

In credit, for example, customers in the lowest band can be auto-approved with minimal friction. Mid bands might require additional documentation or manual underwriting. The highest band might be auto-declined or approved only with collateral or higher pricing. The same idea applies in insurance claims, healthcare triage, or cybersecurity alerts.

Model calibration and decision thresholds that reflect reality

Probability ranges only help if the probabilities are trustworthy. This is where model calibration comes in: when the model says 0.2 probability, roughly 20% of those cases should experience the outcome over time. Calibration translates mathematical outputs into reliable decision inputs.

Decision thresholds then become economic tools. You choose cutoffs by balancing false positives and false negatives in the context of a cost-benefit analysis. What is the cost of wrongly blocking a good customer versus the cost of letting a fraudulent transaction through? Where does the marginal cost intersect the marginal benefit?

Consider a fraud model where the 10–20% risk band actually experiences an observed fraud rate of 9–11%. If further investigation costs $3 per transaction and average fraud loss is $100, you can compute whether additional checks for that band pay off. Over time, you monitor outcomes and re-tune thresholds as behavior and business economics shift.

Encoding risk appetite and tolerance into prediction outputs

In enterprise risk management terms, risk appetite is how much risk you’re willing to take to achieve your goals. Risk tolerance sets acceptable variance around that appetite. A conservative insurer and a growth-oriented fintech may use the same ai risk assessment but make very different choices.

This is where business context meets math. Your organization’s risk appetite shapes where you place decision thresholds, how wide your bands are, and what actions you attach to them. Tight appetites tend to push thresholds lower and actions more conservative; aggressive growth pushes in the opposite direction.

Practically, this requires structured collaboration across risk, operations, and finance. You define initial ranges and actions, run pilots, and review quarterly as loss data, customer behavior, or regulatory expectations evolve. Over time, the probability ranges plus agreed thresholds become a living expression of institutional risk tolerance.

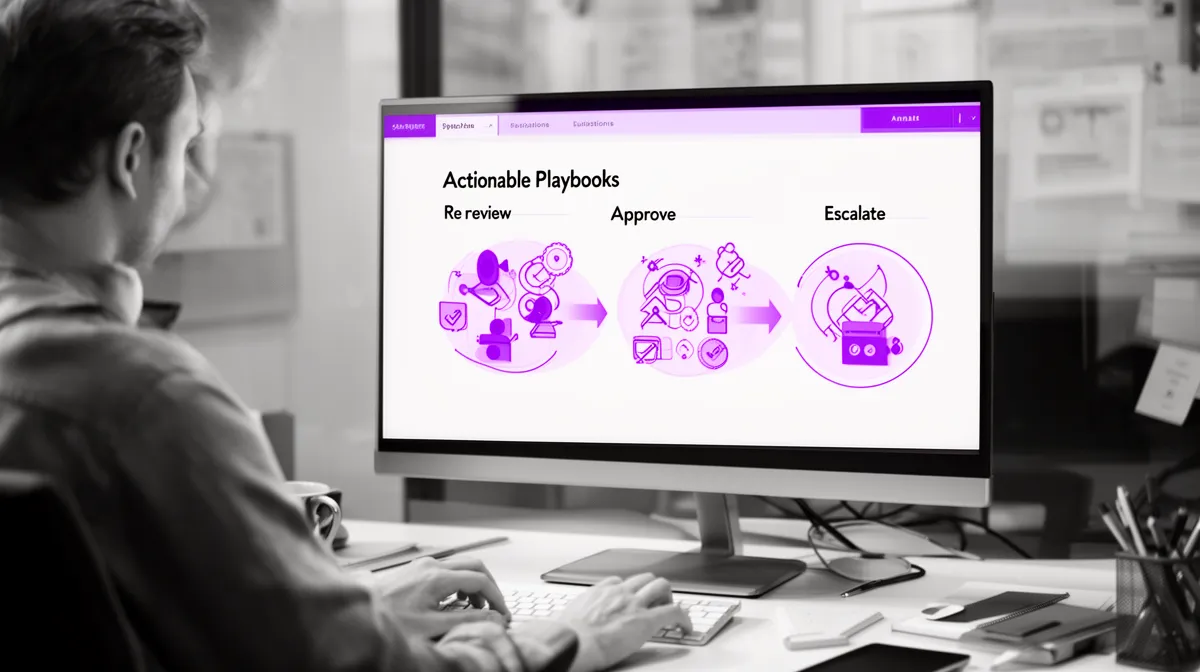

From Prediction to Playbook: Building Actionable Guidance Patterns

Once you have calibrated probability bands, the next challenge is turning them into day-to-day behavior. This is where many risk prediction services stumble: they surface bands (“low/medium/high”) but don’t specify what those labels mean in practice. You need explicit guidance patterns that convert labels into steps.

Translating probability bands into clear operational steps

Guidance patterns are standardized mappings from risk level to actions. For each band, they answer: Should this be auto-approved, manually reviewed, escalated, monitored, or something else? And what exactly does “review” or “escalate” involve?

To generate truly actionable insights, guidance must be concrete and context-aware. “Medium risk – please review” is not enough. You want instructions like: “For this band, verify employment, cross-check income against bank statements, and confirm address history. If all checks pass, approve; otherwise escalate.”

Timeframes and ownership matter too. Who is responsible for each step? What is the SLA? What must be documented for audit or customer communication? Well-defined risk-based decision making patterns incorporate all of this, not just the initial recommendation.

Decision frameworks that pair well with AI-driven risk prediction

Several established frameworks complement AI predictions and make them more robust. Cost-loss and cost-benefit analysis frameworks link decisions to economics: what’s the expected loss avoided versus the cost of extra investigation or friction? Risk matrices visualize severity versus likelihood to prioritize attention.

Decision trees and business rules engine approaches let you encode policy, exceptions, and edge cases alongside model outputs. They’re especially powerful when you want to combine rules (“no approvals from sanctioned countries”) with risk scores (“high-risk applicants require senior sign-off”). Critically, these frameworks anchor decisions in policy and economics, not just guesswork.

From there, you can decide where to use full automated decisioning and where to keep humans in the loop. Low-risk bands might be auto-cleared to reduce cost and latency. Higher-risk or high-impact scenarios (e.g., large loans, sensitive medical decisions) might demand human review supported by clear guidance patterns.

Guidance patterns that support both automation and human judgment

Automation and human expertise are complements, not substitutes. You want guidance patterns that support both “hard” automation rules and “soft” checklists for analysts, underwriters, or investigators. This is where a true decision support system shines.

For low-risk fraud alerts, the pattern might say: “Auto-approve if amount < $X and customer tenure > Y months.” For mid-risk alerts, the system might surface an analyst checklist plus a short rationale: key features driving the risk, suggested data points to inspect, and recommended actions. High-risk cases might route directly to senior reviewers with pre-filled context.

To keep governance risk and compliance satisfied, you version and govern these guidance patterns like code. Changes are documented, reviewed, and rolled out with clear dates. Over time, this supports explainable decision-making: not just explainable AI at the model level, but also human-readable logic at the guidance level.

Embedding Risk Prediction into Real Operational Workflows

Even the best guidance patterns fail if they live outside day-to-day tools. The core lesson in how to integrate risk prediction services into business workflows is simple: start from the workflow, not the model. Where do decisions actually happen today, and what needs to change for those decisions to improve?

Designing risk prediction workflows around existing processes

Begin with a process inventory: CRM flows, ticketing systems, underwriting journeys, claims processing, collections. For each, map the decision points: where is risk assessed, who acts, what data is visible at that moment, and what SLAs apply. This is your blueprint for embedding predictive analytics into real operational workflows.

Then, design around minimal friction. Instead of forcing users to log into a separate risk dashboards tool, surface the risk band and recommended action inside the system they already use. For sales, that might be account pages; for support, the case view; for finance, the approval queue.

For example, integrating a decision-supporting risk engine into a CRM can show relationship managers the current risk level, the logic behind it, and the “next-best action” (e.g., request updated financials, offer a modified product) directly on the account record. This is how you move from real-time risk monitoring as a report to real-time risk as a behavior change.

Integrating with business systems and rules engines

Practically, how to integrate risk prediction services into business workflows comes down to APIs and orchestration. Common integration targets include CRM, ERP, case management systems, underwriting platforms, and payment gateways. A central business rules engine often orchestrates how model outputs interact with policy, exceptions, and overrides.

Consider a payment gateway that calls a risk prediction API for every transaction. The model responds with a probability and band. The rules engine then applies policy: auto-approve low risk, challenge medium risk with 3D Secure, hold high risk for review. These are classic automated decisioning pipelines that embody your enterprise risk management posture.

Latency and throughput matter. Some use cases require sub-200ms responses; others can tolerate hourly or daily batch. Being explicit about these constraints early is central to designing robust ai integration services and ensuring your enterprise risk prediction platform with decision framework integration actually fits production needs.

Ensuring traceability, auditability, and compliance

Any serious risk system must be able to answer a simple question months later: “Why was this decision made?” That means logging the prediction, the probability band, thresholds in force at the time, rules fired, and actions taken, per case. Without this, your governance risk and compliance narrative will be fragile.

Regulators have already highlighted failures where automated risk scoring lacked transparency or governance—for instance, controversial credit-scoring or social-welfare algorithms that impacted vulnerable groups without clear explanations. Strong model interpretability and risk policy automation discipline are now table stakes, not nice-to-haves.

Explainable AI techniques such as SHAP or LIME (see, for example, research from the Nature Machine Intelligence community) can help. But explanation must be coupled with narrative: concise, human-readable reasoning in the interfaces. When a regulator or internal auditor asks why a claim was denied, you want logs that show the model prediction, applicable thresholds, rules fired, and the reviewer’s notes—all in one coherent trail.

Evaluating Vendors: Choosing Decision-Supporting Risk Prediction Services

Once you see the difference between dashboards and decision engines, it completely changes how you evaluate vendors. The core question becomes: are you buying a score generator, or an ai risk prediction service with decision support? This section will help you assess top risk prediction vendors for operational decision making through that lens.

Questions to separate score generators from decision engines

When you ask how to choose risk prediction services that guide decisions, start with pointed questions. First: “How do your risk prediction services map probability ranges to specific actions?” If the answer is “we leave that to the client,” you’re probably looking at a score generator.

Second: “What decision frameworks are built in—do you support cost-loss analysis, decision trees, and configuration of business rules?” Third: “How do you help us encode and adjust risk appetite and SLAs over time?” You want concrete examples of playbooks, rules, and workflow integrations, not just model performance slides.

Finally, ask: “What is a decision-supporting risk prediction service in your view? Can you show us an end-to-end demo where a front-line user takes action based on your system’s guidance?” The clarity of their answer will reveal whether they truly belong among the top risk prediction vendors for operational decision making.

Capabilities that matter: from calibration to governance

Capabilities that actually drive value go beyond algorithms. You want calibrated risk prediction models, configurable bands and decision thresholds, a robust business rules engine, and first-class support for explainability, logging, and monitoring. These are table stakes for any enterprise risk prediction platform with decision framework integration.

Look for support to encode risk appetite, SLAs, and compliance constraints into the system, not into ad hoc spreadsheets. Also ask about governance: versioning of rules and playbooks, change approval workflows, and traceability. Without strong governance risk and compliance features, you’ll struggle the first time regulators or internal audit ask hard questions.

Equally important is vendor support for change management and training. The best risk prediction service for actionable risk insights recognizes that behavior change is the hard part. You should see structured onboarding for analysts and front-line teams, with guidance on interpreting signals and interacting with the decision support system.

Metrics to prove that risk prediction is improving outcomes

To justify investment and assess ai development roi, you need clear metrics. These usually include loss reduction, incident prevention rates, approval rates, manual review rates, operational cost per case, and customer impact (NPS, churn, conversion). Crucially, they must be measured before and after implementation, or via controlled experiments.

Ask vendors how they’ve measured impact in previous deployments. Good partners will talk about A/B testing or phased rollouts that quantify incremental value. Industry reports—from firms like McKinsey or Deloitte on AI-driven risk programs—are full of case studies where structured predictive risk analytics reduced false positives or improved capture rates; use them as benchmarks when you set expectations.

Finally, ensure ongoing real-time risk monitoring of both model and decision performance. Drift, changing customer behavior, or new fraud patterns will erode performance if you treat the system as static. A strong vendor will include monitoring and scenario analysis to keep thresholds, playbooks, and policies aligned over time.

How Buzzi.ai Builds Decision-Enabling Risk Prediction Services

At Buzzi.ai, we’ve built our approach around one idea: start with decisions, not models. Our AI-powered predictive analytics and forecasting services are designed as decision engines—ai risk prediction services with decision support that fit your workflows, policies, and governance structures.

Discovery and alignment around decisions, not just models

Our AI discovery and solution design process begins with a simple map: what are your highest-impact risk decisions, and how are they made today? We talk to risk, operations, analytics, and compliance stakeholders to understand workflows, data sources, ai risk assessment requirements, and constraints.

Instead of asking “What model should we build?”, we ask “What decision do we want to change, and under what conditions?” That shift leads to clearer requirements for ai risk prediction services with decision support: which outcomes matter, what risk appetite looks like, and how guidance must appear in tools people already use.

For example, in a claims context, discovery might reveal that the real challenge is not detecting suspicious claims, but ensuring consistent handling and documentation across adjusters. That insight shapes the playbooks, workflows, and interface design we propose, not just the choice of algorithm.

Architecture: from calibrated models to rules and guidance

Our architectures follow a common pattern: data ingestion; calibrated risk prediction models; a configurable rules and guidance layer; and tight integration into existing systems. The result is a robust decision support system that behaves like an internal decision engine, not a black-box API.

We combine models with a business rules engine that encodes policy, exceptions, and regional variations. On top of that, we build a guidance layer that translates probability bands into specific actions and SLAs, surfacing them in your CRM, case management tools, or risk dashboards. Explainable AI techniques help us generate business-friendly narratives so users understand why the system is recommending something.

A typical decision flow looks like this: data enters → model estimates risk probability → case falls into a band → the rules engine applies policies → the guidance layer generates concrete instructions in the user’s workflow. From the user’s perspective, they see a clear recommendation with reasoning, not a cryptic score.

Ongoing monitoring, governance, and ROI optimization

Implementation is the start, not the finish line. We monitor decision quality over time, not just model metrics. Are losses decreasing? Are manual reviews optimally allocated? Are we hitting the intended balance between risk mitigation and customer experience? This is how we help you maximize ai development roi.

On the governance side, we support logging, audit trails, and versioning of models, rules, and playbooks. That ensures strong governance risk and compliance posture: you can always reconstruct why a decision was made and what configuration was in force at the time. It also supports safe experimentation and controlled evolution.

Lastly, we run regular scenario analysis and threshold tuning sessions with clients. As your data and risk appetite change, we adjust probability bands, SLAs, and guidance patterns. For many clients, these periodic reviews are where the biggest value emerges—small policy shifts that significantly improve both financial outcomes and customer experience.

Conclusion: Turn Risk Prediction into a Decision Engine

Most risk prediction services still stop at scores and charts, leaving front-line teams to improvise. The organizations that see real value treat risk prediction as one layer in a broader decision engine that translates calibrated probabilities into consistent, auditable actions. When you make that shift, you stop asking “Is the model accurate?” and start asking “Are we making better decisions?”

Decision-supporting risk prediction couples probability ranges with thresholds, guidance patterns, workflow integration, and strong governance. It encodes risk appetite, supports explainable AI, and ties directly to business outcomes like loss reduction and customer satisfaction. That’s the bar you should hold vendors—and internal teams—to.

If you want to move from awareness to action, start by identifying one high-impact risk decision area and assessing whether your current tools truly guide that decision. If the answer is no, we’d be happy to explore what a decision-centric service could look like for you. Learn more about our approach to AI-powered predictive analytics and forecasting services, or reach out to discuss a tailored design for your workflows and governance needs.

FAQ: Decision-Supporting Risk Prediction Services

What are risk prediction services and how are they different from basic risk scoring tools?

Risk prediction services are end-to-end capabilities that ingest data, run risk prediction models, and surface outputs directly into business workflows. They go beyond simply assigning a risk score by connecting those scores to thresholds, playbooks, and automation rules. Basic scoring tools stop at the number; robust services help you decide what to do with it, consistently and at scale.

Why don’t raw risk scores or dashboards lead to better risk decisions on their own?

Raw scores and dashboards create awareness but don’t close the gap to action. Humans struggle to translate abstract values like “0.63 risk” into clear, repeatable choices, so they fall back on intuition and local norms. Without explicit guidance patterns and workflow integration, you end up with inconsistent decisions, limited auditability, and under-realized value from your models.

How should a modern risk prediction service express probability ranges to support decisions?

A modern service should use calibrated probability ranges (bands) rather than a single cutoff. Each band—such as 0–5%, 5–20%, 20–50%, and 50%+—should map to specific actions or playbooks with defined SLAs and owners. This approach supports risk stratification, richer risk mitigation strategies, and ongoing tuning as loss data and business conditions change.

What does it mean for a risk prediction service to provide actionable guidance instead of just awareness?

Actionable guidance means the system tells you not only the risk level but also what to do next, by whom, and by when. For each risk band, it should specify whether to auto-approve, manually review, escalate, or monitor, along with concrete steps and documentation requirements. This turns predictive risk analytics into a practical decision support system rather than a passive reporting tool.

How can we connect specific risk thresholds to clear actions, playbooks, or automation rules?

The process starts with defining calibrated thresholds that reflect your risk appetite and cost-benefit trade-offs. From there, you design playbooks that map each band to actions, SLAs, and ownership, and encode those into a business rules engine or workflow automation layer. Over time, you refine thresholds and rules based on outcome monitoring, experiments, and feedback from front-line teams.

Which decision frameworks work best with AI-driven risk prediction models?

Frameworks like cost-loss and cost-benefit analysis, risk matrices, decision trees, and rules engines pair particularly well with AI predictions. They help quantify trade-offs between false positives and false negatives and ensure decisions are grounded in policy and economics rather than intuition. Many organizations also leverage enterprise risk management frameworks to align thresholds and playbooks with broader governance and compliance objectives—for example by working with partners like Buzzi.ai through our predictive analytics and forecasting services.

How do we integrate risk prediction services into existing business workflows and systems?

Integration usually involves APIs, event streams, and a rules or orchestration layer that connects the risk engine to systems like CRM, ERP, case management, or payment gateways. The key is to surface risk bands and guidance directly in the tools where users already make decisions, minimizing friction. A good implementation also ensures logging, monitoring, and explainability are built-in for traceability and regulatory comfort.

How can we encode our organization’s risk appetite and tolerance into a risk prediction service?

You do this by jointly defining probability bands, thresholds, and associated actions that reflect how much risk you’re willing to accept for given rewards. Risk, operations, and finance teams collaborate to set initial bands, SLAs, and escalation paths, then review them regularly as losses, regulations, or strategy change. Over time, these configurations become a living, operational expression of your risk appetite and tolerance.

What metrics show that a risk prediction service is actually improving decisions and outcomes?

Useful metrics include loss or incident reduction, fraud capture rates, false positive and false negative rates, manual review volumes, operational cost per case, and customer impact measures like approval rates, NPS, and churn. You should compare these metrics before and after implementation, or through A/B tests where possible. Continuous monitoring will help detect when models, thresholds, or playbooks need adjustment to stay aligned with evolving risk and business conditions.

How does Buzzi.ai design and implement decision-supporting risk prediction services in practice?

We start with discovery around key decisions and workflows, then design calibrated models, probability bands, and rules that reflect your risk appetite and policies. From there, we integrate a guidance layer into your existing tools, with strong logging, explainability, and governance. Finally, we support ongoing monitoring, scenario analysis, and threshold tuning to ensure your risk prediction service continues to deliver measurable, decision-level ROI.